While much has changed in the world of tax recovery in GlobeTax’s 26 years, a few truths remain constant:

- Beneficial owners want tax relief entitlements on foreign income;

- Withholding agents and tax authorities want to know the identity of beneficial owners before granting tax entitlements through relief at source or long form processes, respectively;

- Financial institutions want to minimize cost and risk when conducting global operations. In most cases, this involves co-mingling assets in omnibus accounts.

The third point is critical, as it often inhibits the first two. While efficient for financial intermediaries, omnibus accounts impede the ability of withholding agents and tax authorities to identify both the ultimate beneficiary and whether they qualify for treaty benefits. Without such visibility, tax treaty entitlements cannot be granted, disheartening investors. The central issue in the tax space thus becomes: is it possible to resolve the omnibus dilemma, reconciling the needs of all three groups?

Advantages and Limitations of Omnibus Accounts

Combining accounts to obtain processing and cost efficiencies is a main factor driving the prevalence of omnibus accounts. Indeed, the vehicles are the most economical way to structure custody assets. Because only one account is needed to facilitate the trading and maintenance of assets for many investors, account onboarding and maintenance fees are sharply reduced. By contrast, opening a segregated account for every client at every sub-custodian in the custody network would require enormous labor and expense for reporting, reconciliation, and data storage. The opacity of omnibus accounts yields additional commercial benefits. It prevents other custody network participants from poaching clients, ensuring maintenance of AUM.

Despite these merits, the opaque and co-mingled nature of the accounts presents drawbacks. First, issuers need to understand their global shareholder base to meet requirements for corporate communications and proxy voting, a task rendered challenging when information is held in omnibus accounts. Likewise, withholding agents need to understand ultimate beneficiaries, not only to grant proper tax relief, but also to combat money laundering, terrorist financing, and sanctions requirements. These burdens are shared by tax authorities and financial institutions, who must confirm beneficial ownership to assess standard post pay date reclaims and ensure compliance with AML, KYC, and KYCC requirements. Lastly, in the aftermath of Lehman Brothers, MF Global, and Madoff, etc., larger investors are shunning the account structure, instead demanding clearer asset segregation to protect against forced liquidation in the event of intermediary insolvency.

Further Constraints

The use of omnibus accounts is further constrained by national rules, counterparty requirements, and treaty stipulations. Many countries have specific laws governing the use of omnibus accounts. Some Central Securities Depositories—Norway or China, for instance—require the use of segregated accounts for domestic participants and/or investors. Counterparties, too, maintain specific mandates: some accept rate-pool accounts, others demand segregated. Lastly, treaties often influence the use of different account types. As relief at source requires passing information through the custody chain within very narrow windows – sometimes mere hours – the process often obviates the use of omnibus accounts in practice, as designated intermediaries cannot quickly pierce them to understand the underlying owners.

Due to these complex (and often conflicting) requirements, it is no wonder that intermediaries aggregate clients into a single account, subjecting all beneficial owners to withholding at the full rate. Increasingly, however, institutional investors are clamoring for tax relief, forcing custody chain participants to find a solution, despite their low margins and growing regulatory burdens.

So what is a custodian to do?

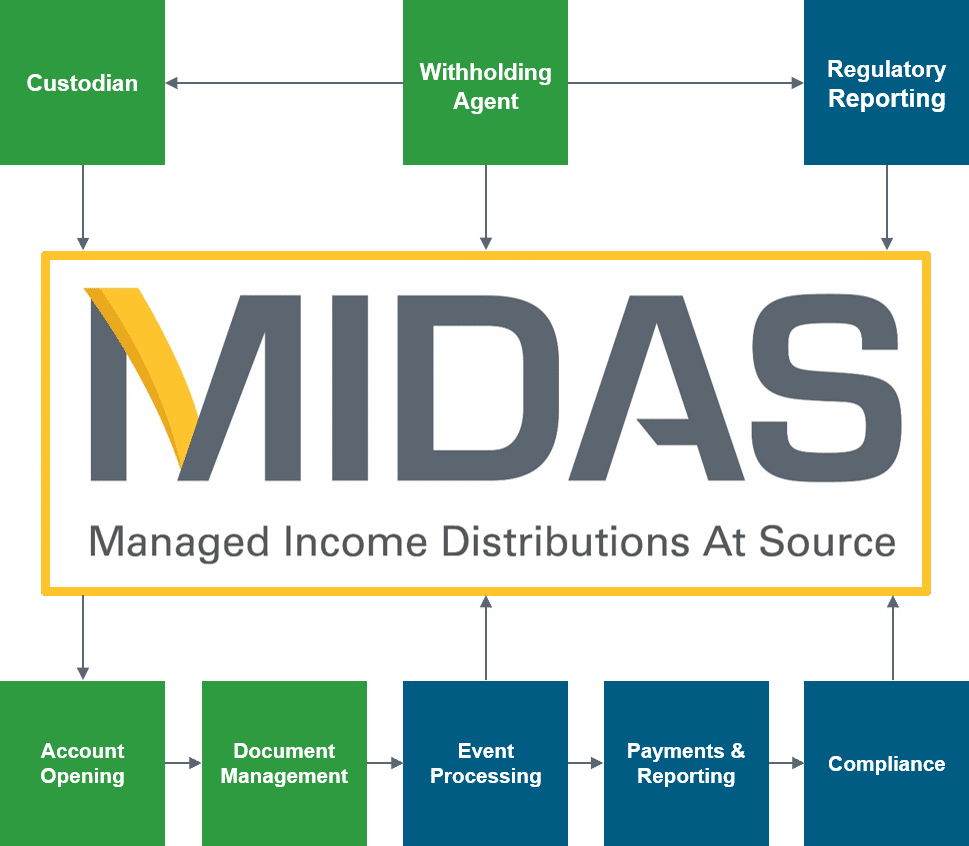

MIDAS®: An Omnibus Account Solution

GlobeTax’s MIDAS service helps resolve the omnibus dilemma. Each user type simply plugs into the centralized platform to both provide and access the information they need. MIDAS maintains omnibus account rules and beneficial owner documents, and features customizable views so each custody chain participant can understand the action they must take to play their role in the withholding tax recovery process. Moreover, information from one link in the custody chain is shielded from others in the chain, allowing each financial institution to protect its customers.

Centralized Rules

Financial intermediaries need an easy way to understand when they can – and cannot – use omnibus accounts. MIDAS maintains and provides up-to-date rules for each market and each entity in the custody chain, from withholding and transfer agents to local sub-custodians to global custodians to regional banks and brokers. These rules delineate the use of segregated, rate pool, and blended rate accounts both up and down-stream, so financial intermediaries can devise the most optimal, cost-effective way to organize their clients participating in tax relief across all markets.

Centralized Documents

Once a financial institution understands account type requirements, the next step is understanding the document requirements and ensuring that the requisite information is on file for each underlying investor. As the custody network is presently organized, multiple sets of documents must be maintained at different FIs; the intermediaries do not willingly share client information with each other.

MIDAS resolves this issue by maintaining documentation in a central repository. All FIs are granted a unique and secure view into the platform, and will be able to access and verify that the documentation is on file for each omnibus participant. Such centralization eliminates the issue of document redundancy and provides a ‘master copy’ to ensure that all investor information remains consistent throughout the custody chain.

Customized Views

Each user type will experience a different view upon logging into the portal. For instance, a tax authority performing an audit can look through all omnibus accounts to ensure all necessary documentation is present for all investors. By contrast, the omnibus account manager can similarly verify requirements without seeing information of any omnibus accounts up or downstream. Such flexible, multi-faceted permissioning ensures that the original purposes of the omnibus account—cost efficiency and secrecy maintenance—are upheld without depriving investors of their tax entitlements.

The Ubiquitous Omnibus

Due to their cost advantages and utility, omnibus accounts are likely not going away any time soon. As a result, it is vital to find a solution that balances the requirements of all parties—custodians, tax authorities, withholding agents, and investors. In the complicated world of tax recovery. MIDAS is that solution.